June 08, 2001

Data Do Not Always Support Conventional Wisdom

It’s amazing what one can learn by looking up the numbers. As readers of this column know, often the numbers do not square with conventional wisdom or our perceptions.

Example 1: Contrary to presumptions, exports have NOT been the driving force of major crop demand growth. Over the last two decades, exports for most major crops have had flat to declining trends.

Example 2: Although cited as the reason for recent lack luster U.S. export demand, low prices, and why Freedom to Farm has sputtered, the Asian Crisis did not precipitate a decline in the growth of grain domestic demand, either worldwide or in foreign countries (worldwide less the U.S.). In fact, worldwide and foreign domestic grain demand grew at a faster pace during this period than earlier in the decade. The primary problem was excessive output—in and outside the U.S.

Example 3: The total world harvested acreage for the eight major crops has declined somewhat in recent years. It would be natural to think that the low prices of recent years have persuaded our export competitors and/or export customers to reduce acreage. The acreage numbers tell a very different story. Most of the grain acreage decline occurred in three former Soviet Union countries in response to drastic reductions in livestock numbers and the turmoil of shifting to a more market oriented economy. Our export competitors, on the other hand, experienced a 36 million acre increase in harvested acres of the eight major crops (corn, soybeans, barley, oats, cotton, grain sorghum, rice, and wheat) since the mid-1990s. This increase amounts to nearly half of the U.S. corn or soybean acreage.

While looking up the numbers for the Asian Crisis effect, we saw other data that brought into question another conventional wisdom. Let’s call it example 4.

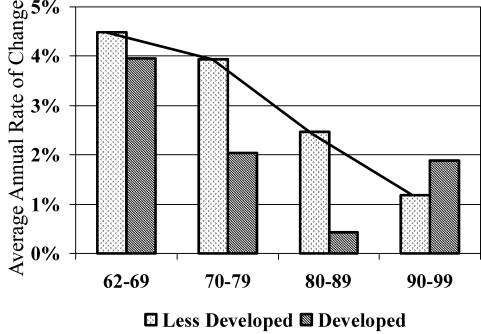

The conventional wisdom is that domestic demand grows faster in less developed (developing) than in developed countries. Also, less developed countries often experience less growth in domestic agricultural production than developed countries. The implication being that less developed countries hold the most promise as growth markets for agricultural exports.

As figure 1 shows, using USDA Production, Supply & Demand data, the average annual rate of growth in domestic demand for total grains and total seeds in less developed countries in the 1970s was twice the growth rate in developed countries and four times as great in the 1980s. But in the 1990s, domestic demand growth increased at a faster rate in developed than developing countries.

Figure 1. Average annual rate of change in developed and less developed countries’ domestic demand for grains and seeds for the 60s, 70s, 80s, and 90s. Total grains includes wheat, ride, corn, barley, sorghum, rye, oats, millet, and mixed grains. Total seeds includes soybeans, cottonseed, rapeseed, peanuts, sunflowerseed, copra, and palm kernel.

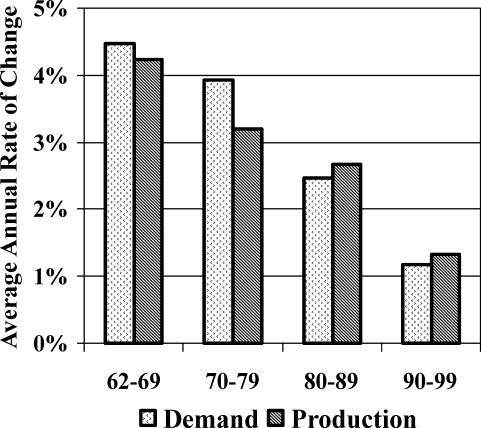

Note that the average annual rate of growth in domestic demand for grains and seeds has decreased each of the decades since the sixties (line in figure 1). The annual average growth rate for production of grains and seeds in developing countries has also trended downward since the 1960s (the second bar in figure 2). A similar downward trend in production growth is evident for developed countries with the rate of growth averaging about one-half of one percent higher than for developing countries during each of the decades (not shown on the graphs).

Figure 2 has the average annual rates of growth of both demand and production in developing countries by decades. Notice that the average rate of growth of production in developing countries exceeded the rate of growth in demand in the 1980s and the 1990s.

So example 4 of when conventional wisdom does not match the data is: Despite expectations to the contrary, developing countries are not showing promise as a surging source of export growth for grains and soybeans in the years ahead. Rather, the data show that domestic demand for grains and soybeans haas declined from an average growth rate of 4.5% in the 1960s to slightly above 1 percent in the 1990s. Furthermore, domestic production of grains and seeds is increasing faster than demand.

Figure 2. Average annual rate of change in less developed countries domestic demand and production for grains and seeds for the 60s, 70s, 80s, and 90s. Total grains includes wheat, ride, corn, barley, sorghum, rye, oats, millet, and mixed grains. Total seeds includes soybeans, cottonseed, rapeseed, peanuts, sunflowerseed, copra, and palm kernel.

With their demand growing slower and with less developed countries providing a greater share of their needs, it is probably unwise to base farm prosperity expectations on accelerated growth in crop exports to less developed countries.

Daryll E. Ray holds the Blasingame Chair of Excellence in Agricultural Policy, Institute of Agriculture, University of Tennessee, and is the Director of the UT’s Agricultural Policy Analysis Center. (865) 974-7407; Fax: (865) 974-7298; dray@utk.edu; http://www.agpolicy.org.

Reproduction Permission Granted with:

1) Full attribution to Daryll E. Ray and the Agricultural Policy Analysis Center, University of Tennessee, Knoxville, TN;

2) An email sent to hdschaffer@utk.edu indicating how often you intend on running Dr. Ray’s column and your total circulation. Also, please send one copy of the first issue with Dr. Ray’s column in it to Harwood Schaffer, Agricultural Policy Analysis Center, 310 Morgan Hall, Knoxville, TN 37996-4500.